Move to Korea

Cost of Living in Seoul for Foreigners (2026): A Real Monthly Budget

📈 Trend signal: Cost of living in Seoul for foreigners 2026

Heads up: some links below are affiliate links. If you sign up through them, I may earn a small commission at no extra cost to you. I only point to services I’ve actually used to set up my own life in Seoul.

When I moved to Seoul, every “cost of living” article gave me the same useless answer: “It depends!” Yes, obviously. But I still needed a real number to know whether my salary would survive the month. So here’s the honest version I wish I’d had — a working monthly budget for a single foreigner, whether you’re an English teacher (if you’re still sorting the visa, start with our E-2 visa document checklist), a young professional, or a student.

I’ve split everything into a Low (frugal but comfortable) and Mid (relaxed, some eating out and travel) column, priced in Korean won, with the dollar total at the bottom. Exchange rate used throughout: roughly ₩1,390 = $1 (mid-2026). Prices drift, so treat these as your planning map, not a receipt.

The headline number

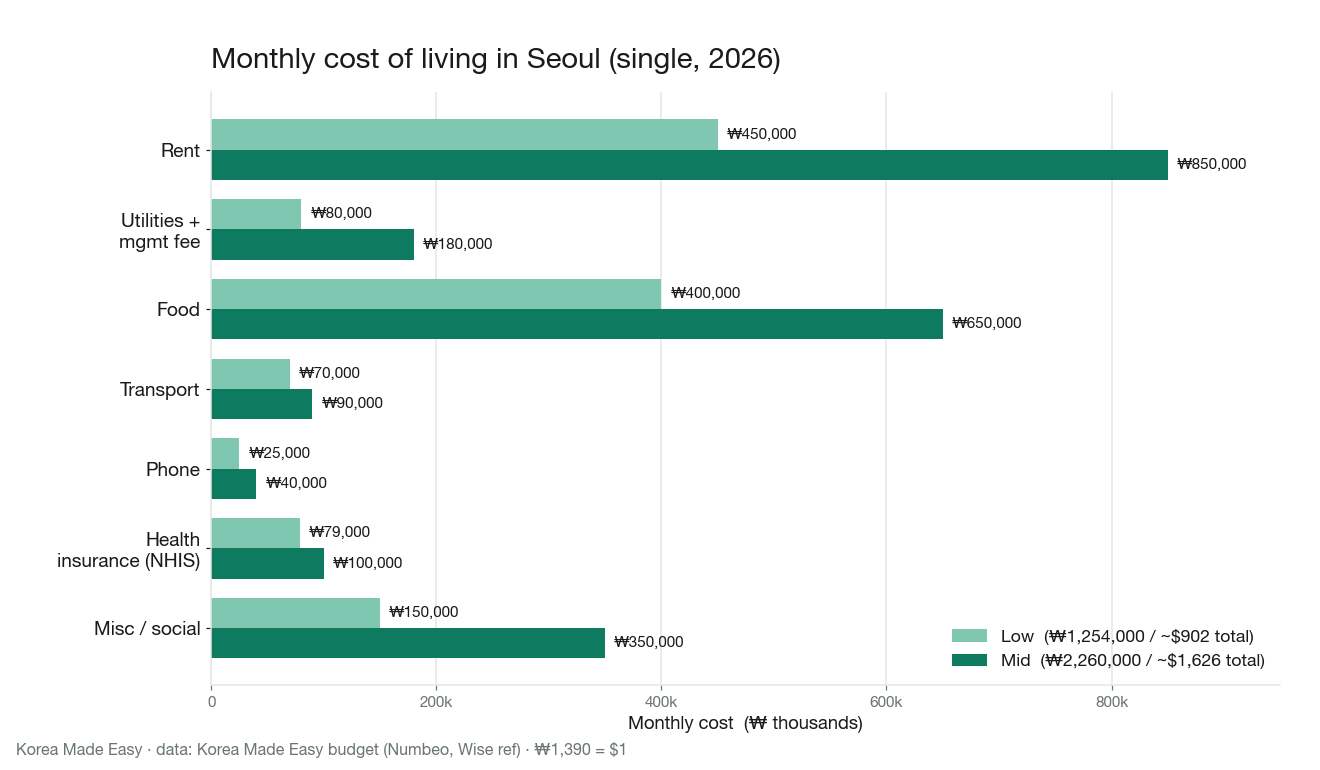

Living on your own in Seoul as a single foreigner realistically costs between ₩1,250,000 and ₩2,260,000 a month — about $900 to $1,630. The low end assumes a goshiwon or share house, cooking most meals, and modest going out. The mid end is a private one-room officetel, a healthy mix of groceries and restaurants, and a social life.

Most people I know land in the ₩1.6M–₩2.0M ($1,150–$1,440) zone once they’ve furnished a place and made friends. Your single biggest lever, by far, is rent — so let’s start there.

Housing: deposits, wolse, and why the system feels weird

The first shock for foreigners is that Korean rent runs on deposits, and they’re big. There are two systems:

- Wolse (월세) — monthly rent, the one you’ll almost certainly use. You put down a deposit (bojeunggeum) of anywhere from ₩5M to ₩10M for a small officetel, then pay rent on top each month. The bigger your deposit, the lower your monthly rent — landlords will negotiate that trade.

- Jeonse (전세) — no monthly rent at all. Instead you hand the landlord a massive lump sum, often ₩100M–₩300M+, which they return in full when you leave. It only makes sense if you have serious capital sitting around, so most newcomers skip it entirely.

Here are the realistic 2026 options, cheapest to priciest:

| Type | Typical deposit | Monthly rent | Best for |

|---|---|---|---|

| Goshiwon (고시원) | ₩0–1,000,000 | ₩350,000–700,000 | Cheapest start; students; passport-only, no ARC needed |

| Share house | 1–2 months’ rent (~₩500K–1M) | ₩400,000–650,000 | Making friends fast; low deposit; short commitment |

| Officetel / one-room (wolse) | ₩5,000,000–10,000,000 | ₩600,000–1,000,000 | Privacy and your own kitchen; young professionals |

| Jeonse (any type) | ₩100,000,000+ | ₩0 | Long stayers with a big cash buffer |

A goshiwon is a tiny furnished room — bed, desk, often a shared or cramped private bathroom — with free rice and ramen in the common kitchen. It’s not glamorous, but it gets you in the door with almost no deposit. A share house buys you a private bedroom plus shared common areas and an instant social circle. A private officetel is the sweet spot most professionals graduate to: a modern studio near a subway station, but budget an extra ₩150,000–₩200,000/month management fee (관리비) that isn’t always quoted upfront.

One warning I give everyone: moving that first deposit into Korea through a normal bank wire will quietly cost you a chunk in fees and a bad exchange rate. I use Wise to send the lump sum at the real mid-market rate.

👉 Move money to Korea with Wise

Food: the cook-vs-eat-out equation

Food is where your habits decide your budget. Cooking at home is genuinely cheap; groceries run ₩200,000–₩400,000/month for one person. The catch is that fresh produce and imported goods are pricey — Korean supermarket produce sits well above the OECD average, so a kilo of beef can hit ₩33,000 and apples ₩11,000/kg.

Eating out, on the other hand, is a bargain by big-city standards. A proper sit-down Korean meal is ₩8,000–₩15,000, a convenience-store meal ₩3,000–₩6,000, and street food ₩2,000–₩5,000. A casual day out — two meals plus a coffee — lands around ₩25,000–₩40,000. My honest advice: cook breakfasts and lunches, eat out for dinner and weekends, and you’ll keep food to roughly ₩400,000 (frugal) to ₩650,000 (comfortable) a month.

Transport: T-money is almost too cheap

Seoul’s public transport is the best deal in your budget. Grab a T-money card, tap in and out, and the base subway/bus fare is ₩1,550 as of 2026. Even commuting twice a day plus weekend trips, I rarely spend more than ₩70,000–₩90,000/month. Transfers between bus and subway are free within the window, which keeps costs down.

If you’re still landing and don’t have your Alien Registration Card (ARC) yet, a T-money card works for anyone — no registration needed — so it’s the first thing to buy at the airport.

Utilities and phone

For a small officetel, expect electricity, gas, water, and internet to total ₩80,000–₩150,000/month, swinging higher in the summer AC season and the deep winter (Korean heating bills are real). In a goshiwon or share house, utilities are usually bundled into your rent — one less thing to manage.

Phone is delightfully cheap if you skip the big three carriers (SKT, KT, LG U+ at ~₩89,000/month) and use an MVNO (알뜰폰) instead. These resell the exact same networks for ₩25,000–₩40,000/month. The one snag: postpaid MVNO plans require your ARC. Before that card arrives, you’ll want a prepaid SIM or, cleaner, an eSIM you activate before you even land — I break down which one to buy in our Korea eSIM guide.

Health insurance: not optional, but reasonable

Here’s one newcomers underestimate: if you live in Korea long-term, National Health Insurance (NHIS) is mandatory. If you’re employed by a Korean company, it’s a payroll deduction — around 7.09% of salary in 2026, split with your employer, so you pay roughly half. If you’re a freelancer, student, or otherwise a regional subscriber, you pay a floor premium of about ₩79,000–₩100,000/month.

It’s worth every won. Once enrolled, a doctor’s visit often costs a few thousand won out of pocket, and Korea’s healthcare is fast and excellent. I’ve budgeted the regional-subscriber figure below; if you’re salaried, your deduction may be similar or a bit higher depending on pay.

The full monthly budget

Putting it all together for a single foreigner in Seoul, 2026:

| Category | Low (₩) | Mid (₩) | Notes |

|---|---|---|---|

| Rent | 450,000 | 850,000 | Low = goshiwon/share; Mid = one-room officetel (wolse) |

| Utilities + management fee | 80,000 | 180,000 | Bundled in goshiwon/share; separate for officetel |

| Food (groceries + eating out) | 400,000 | 650,000 | Cook most meals vs. regular restaurants |

| Transport (T-money) | 70,000 | 90,000 | ₩1,550 base fare, free transfers |

| Phone | 25,000 | 40,000 | MVNO (알뜰폰); needs ARC for postpaid |

| Health insurance (NHIS) | 79,000 | 100,000 | Regional-subscriber floor; salaried is a payroll split |

| Misc / social / leisure | 150,000 | 350,000 | Coffee, nights out, gym, the occasional trip |

| Total (KRW) | ₩1,254,000 | ₩2,260,000 | Single person, all-in |

| Total (USD, ~₩1,390) | ~$902 | ~$1,626 | Your salary needs to clear this |

For context, Numbeo pegs a single person’s non-rent monthly spend in Seoul at roughly ₩1.5M, and Wise’s city guide lands in a similar all-in range — my table just splits it into levers you can actually pull.

How to save the most

If money is tight, attack in this order:

- Rent first. Choosing a goshiwon or share house over a private officetel can cut ₩400,000+/month. Nothing else on the list comes close.

- Cook your weekday meals. Groceries beat restaurants for staples; save eating out for dinners and weekends.

- Go MVNO on your phone. Same network, half the price of the big carriers.

- Live near a subway line, not in a “hot” neighborhood. One or two stops out of Gangnam or Hongdae can drop your rent dramatically for the same commute.

- Move your money smartly. Bad exchange rates on big transfers quietly eat hundreds of dollars — a real mid-market transfer service pays for itself the first time you move a deposit.

FAQ

Is Seoul cheaper than a Western city like London or New York? Yes, noticeably — mostly on rent, transport, and eating out. My all-in ₩1.25M–₩2.26M ($900–$1,630) would be hard to match in central London or NYC, where rent alone often exceeds that. Where Seoul stings is imported groceries and Western products. Day-to-day Korean living, though, is a clear win.

What’s the cheapest realistic way to live in Seoul? A goshiwon (₩350K–₩700K, little to no deposit) or a share house, cook most of your meals, ride the subway with T-money, and use an MVNO phone plan. That combination keeps a single person comfortably near the ₩1.25M ($900) low end.

Do I really need a huge deposit? Not to get started. Goshiwon and share houses take a passport and a small deposit (often ₩0–₩1M), which is exactly why newcomers use them. The big ₩5M–₩10M wolse deposits — and the six-figure jeonse ones — only come into play once you want your own private officetel and have the cash to lower your monthly rent.

That’s the real picture. Seoul rewards people who choose rent wisely and cook a little — do those two things and it’s one of the more affordable major cities you’ll ever live in. When you’re ready to move your first deposit over without losing money to bad bank rates, 👉 move money to Korea with Wise.

Sources

- https://www.numbeo.com/cost-of-living/in/Seoul

- https://wise.com/gb/cost-of-living/south-korea/seoul

- https://allo-korea.com/en/housing-in-korea-guide-2026/

- https://www.haniseoul.com/blogs/korea-health-insurance-nhis-foreigner-guide

- https://www.vianotehub.com/korea-transportation-card-2026/

Search-trend data from Google Trends (KR) and Naver DataLab. This article is independent commentary and is not affiliated with any broadcaster, agency, or the individuals mentioned.